Steiner and Company produces the Profit Maximizer report on behalf of National Pork Board based on information we believe is accurate and reliable. However neither NPB nor Steiner and Company warrants or guarantees the accuracy of or accepts any liability for the data, opinions or recommendations expressed.

Highlights

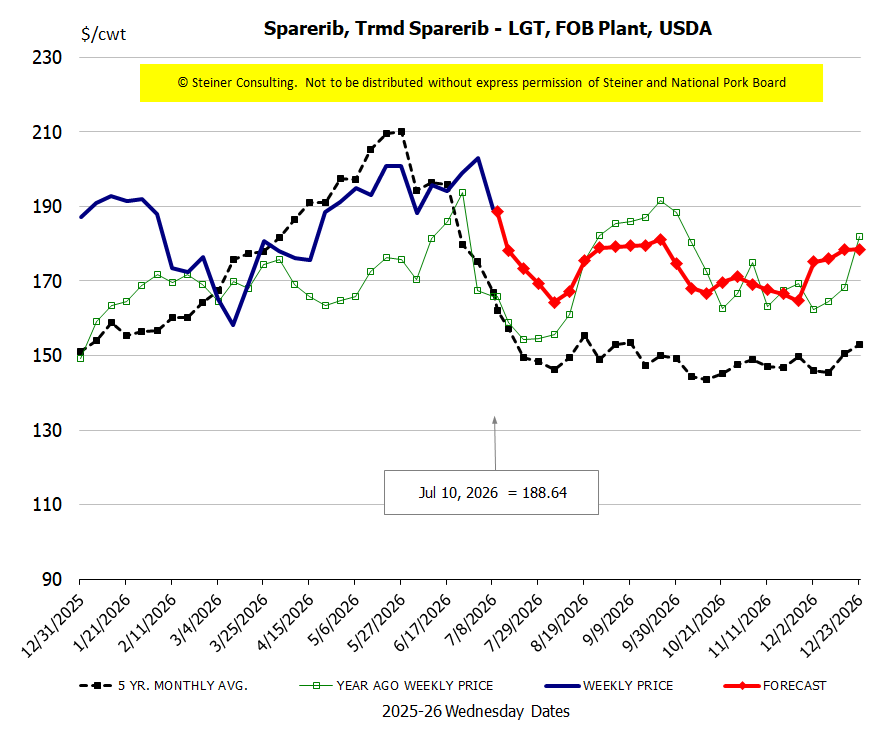

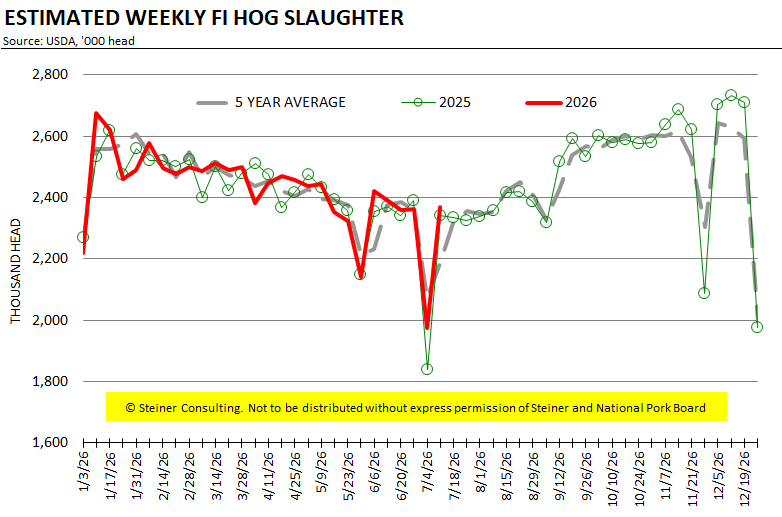

- It is not unusual for processing pork prices to rebound after the holidays as plants return to full production schedules. That combined with two short production weeks has resulted in tighter spot availability and higher prices, especially hams.

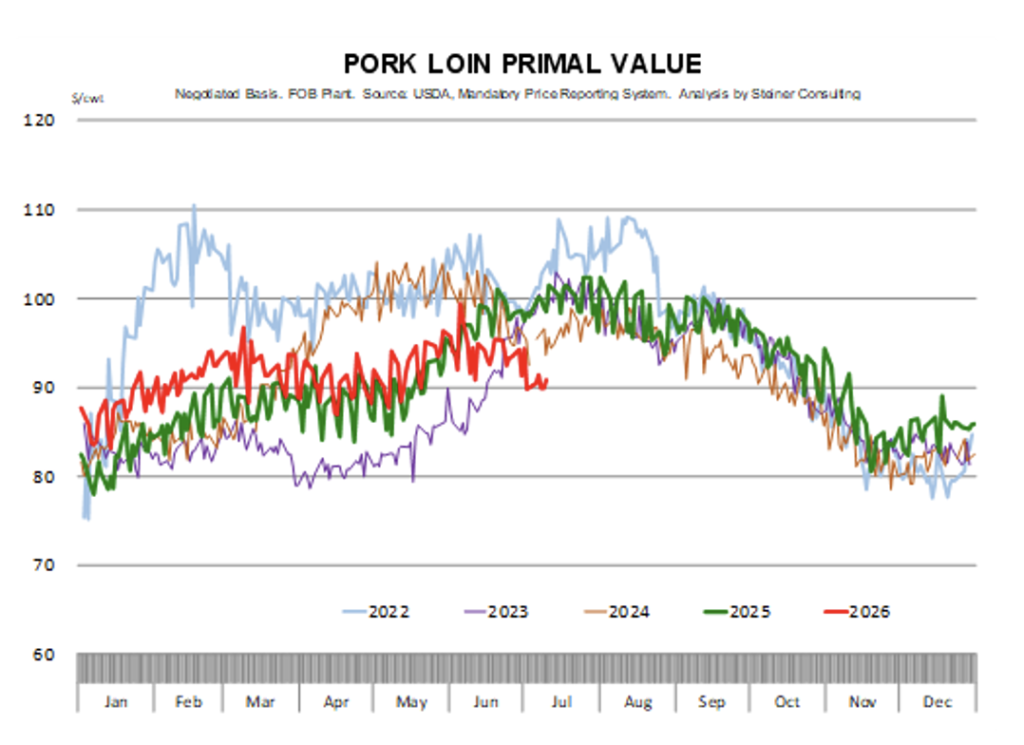

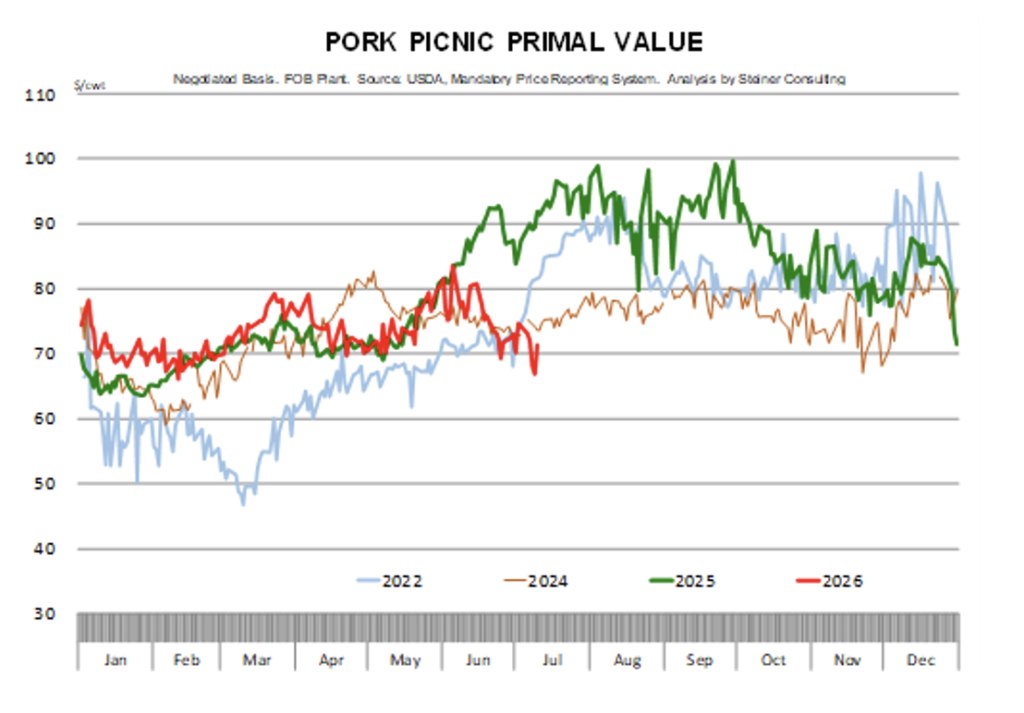

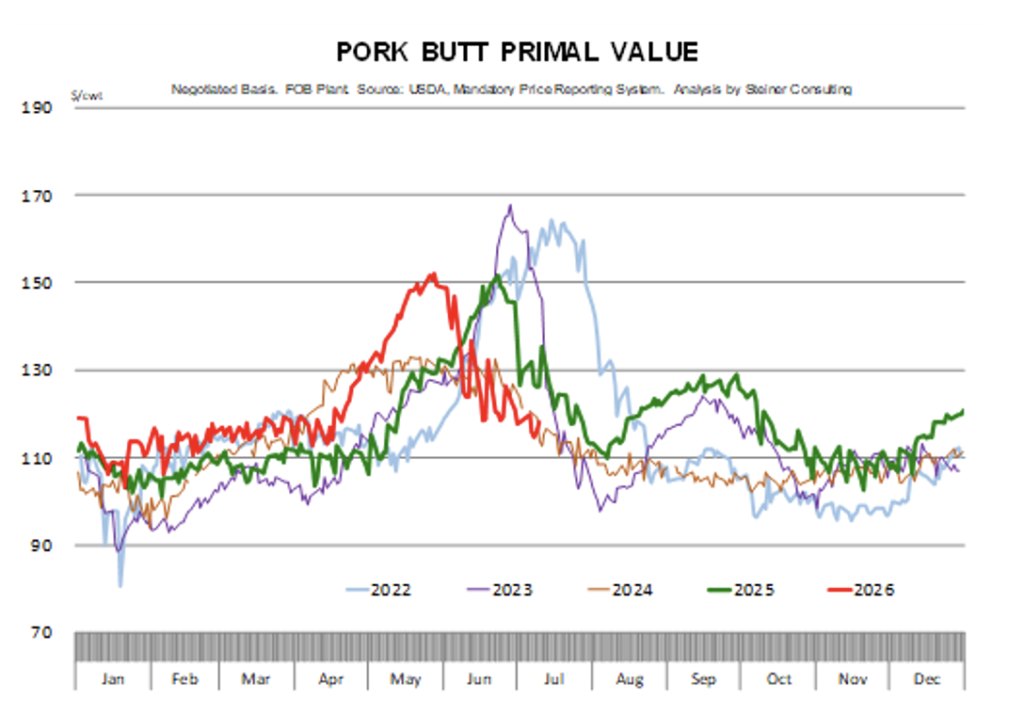

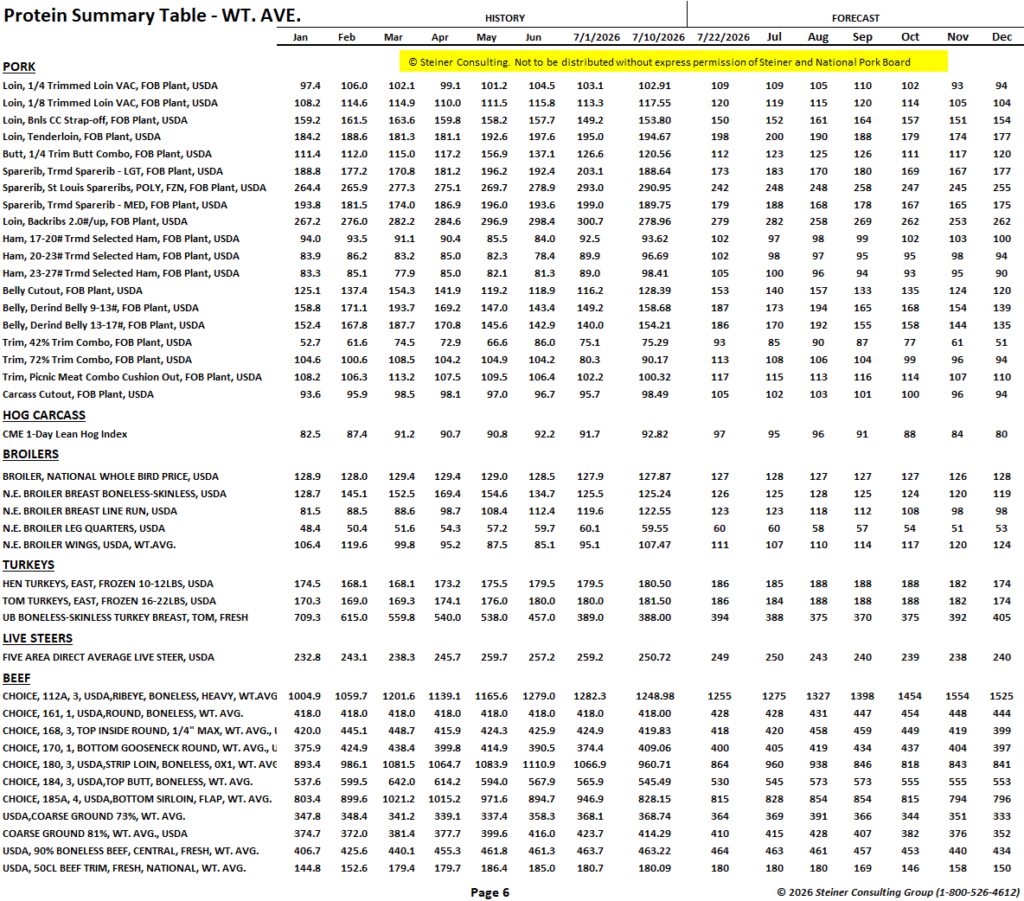

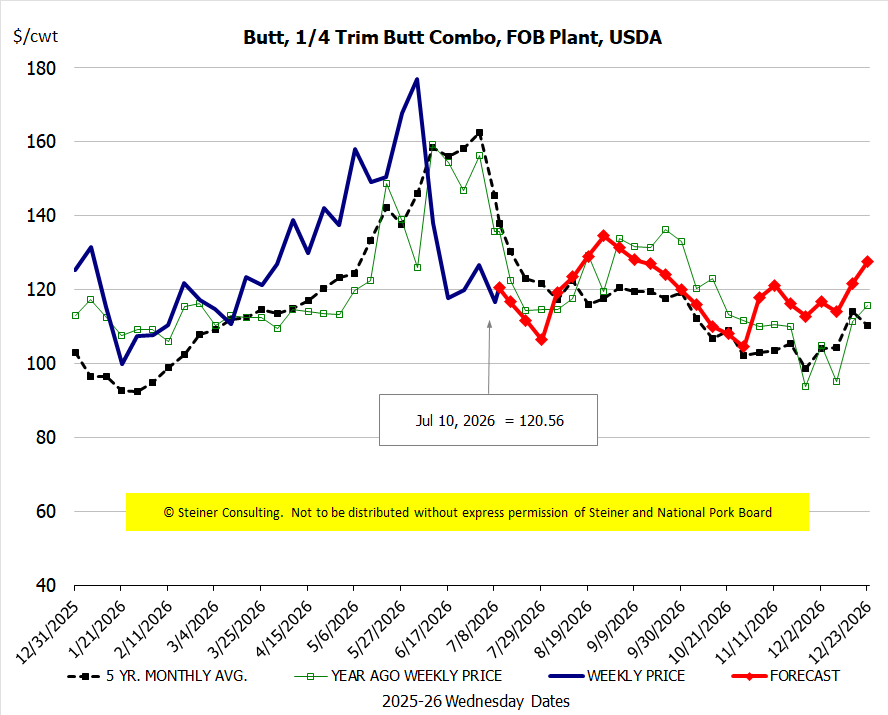

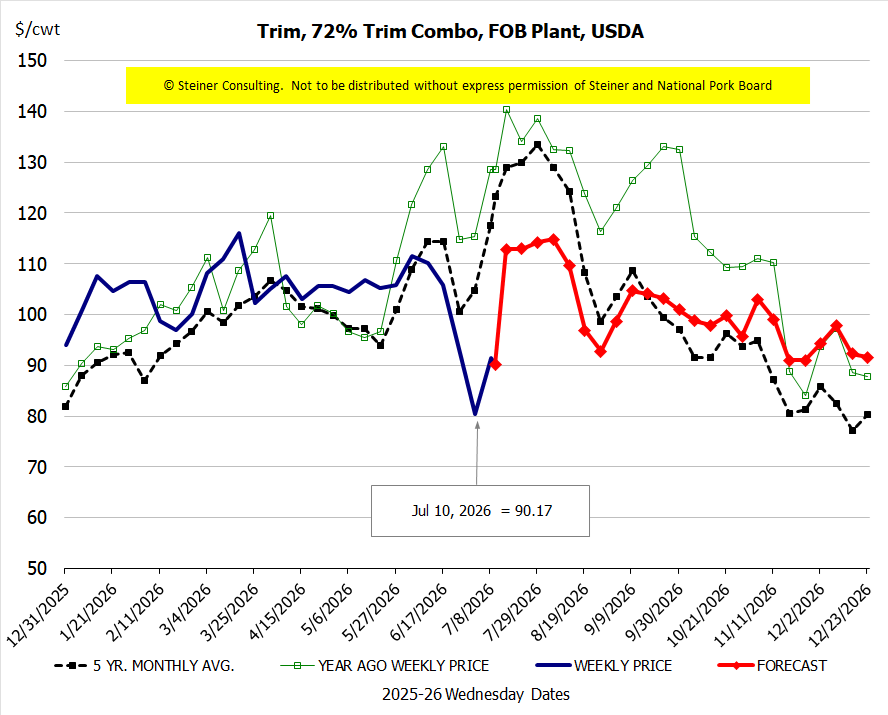

- Fresh pork prices continue to underperform and seasonally prices tend to stay soft through the hot summer months as fresh pork is not a major retail feature. Loins are expected to trade sideways, as weakness in seasonal demand is offset by lower supply. Butts and picnics are also expected to trade sideways while rib prices are expected to trend lower now that peak demand is behind us.

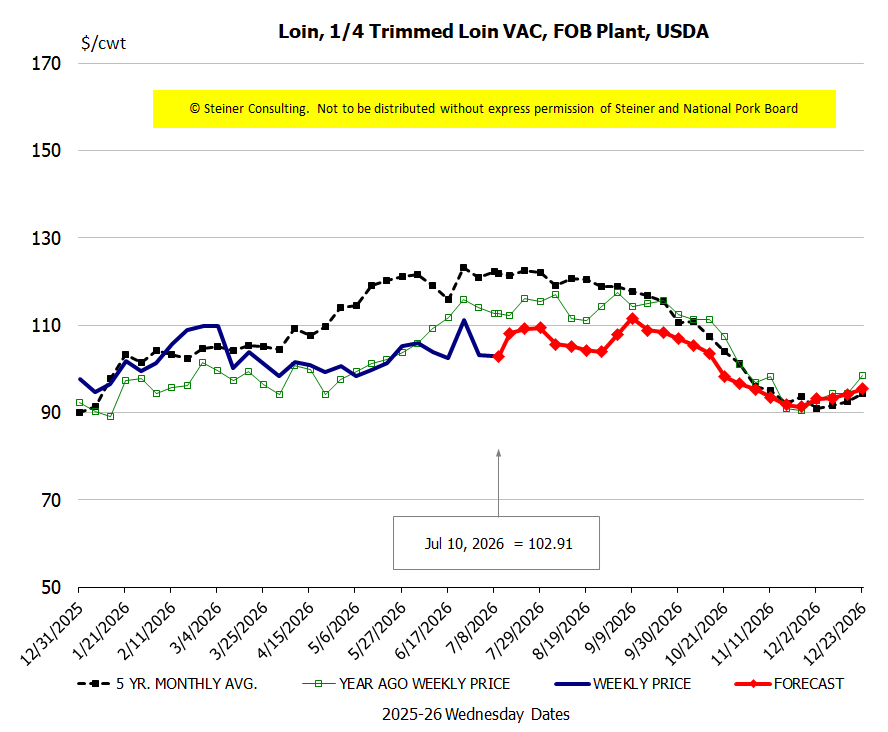

- Processing items are expected to trade firm in the next 4-5 weeks. Carcass weights so far have helped bolster pork supply and remain a wild card due to increasing temps/humidity in key production areas.

Full Report

Fresh Pork Challenges Persist, Limiting the Upside for Pork Prices in Q3

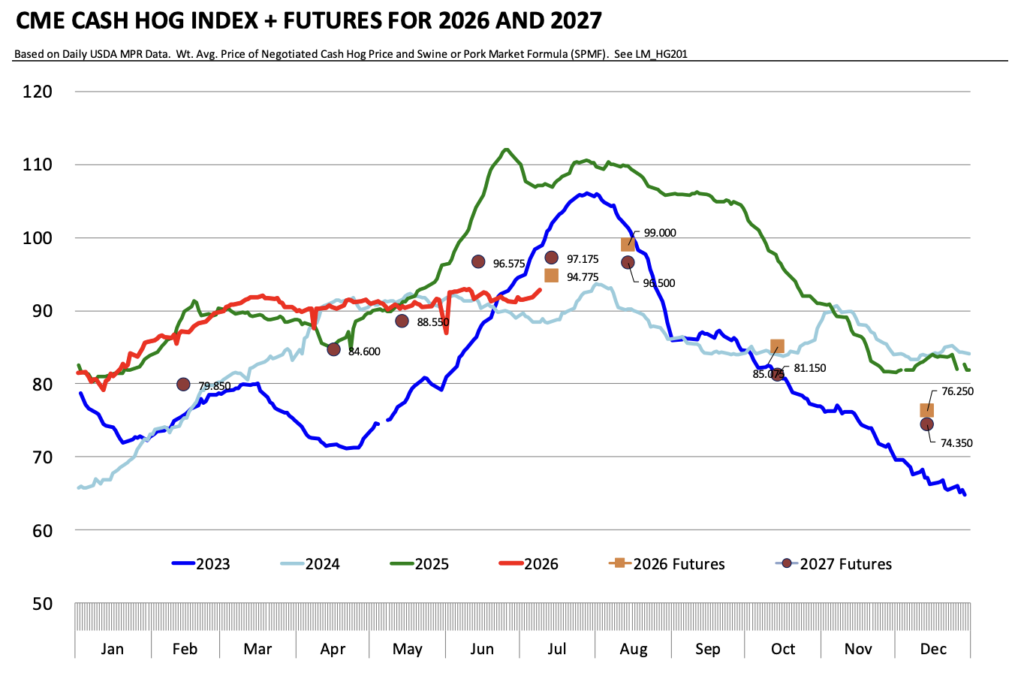

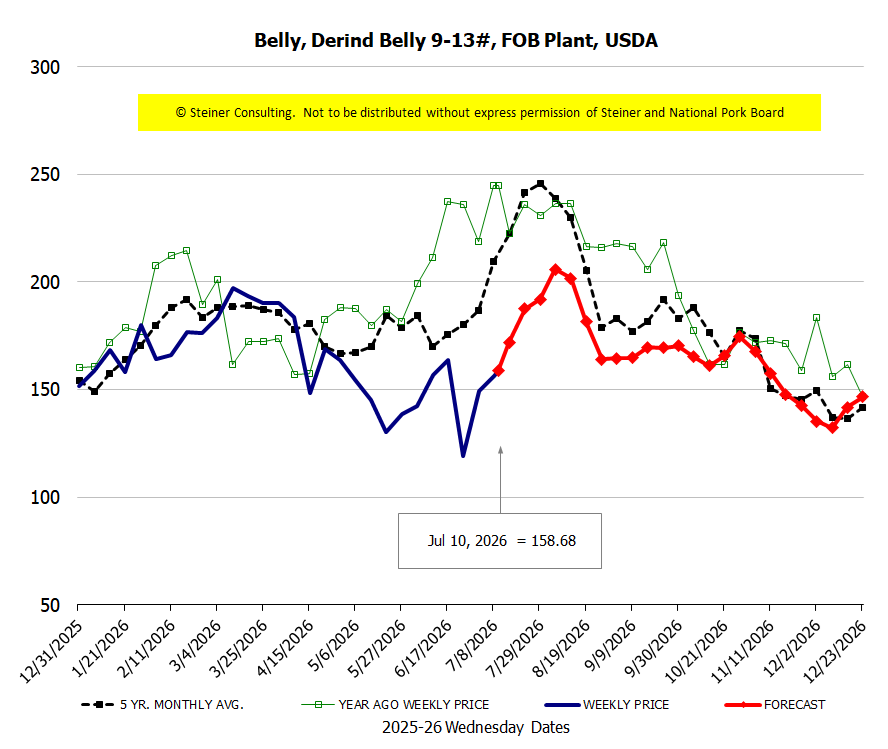

Lean hog futures have rebounded in the last few days as processing items, which have been the primary drag on the cutout in recent weeks, have started to gain traction. The belly primal last week was quoted at $128/cwt, $10.4/cwt (+9%) higher than a week ago. Similarly, the ham primal at $94.9/cwt was up $8.8/cwt (+10%). The gains in hams and bellies added almost $5/cwt to the cutout, although lower prices for other items, especially picnics, offset part of those gains.

As market participants consider the outlook for the nearby August contract and Q4 futures, the price trend for processing items will remain important. However, it is equally important not to lose sight of the other components of the cutout. The loin, pork butt, picnic and rib primals account for a little over half of the cutout’s value, making demand for fresh pork particularly significant. What has been especially disappointing is that despite record high beef prices at retail, fresh pork prices have not benefited much. The hope at the start of the year was that consumers would gravitate toward lower priced proteins, with pork by far offering the best value. However, that expectation failed to recognize some important factors.

First, lower-income consumers have been hit hardest by higher fuel prices and also tend to account for a disproportionate share of pork sales. Those consumers are not deciding between pork and beef but rather how much they are willing to spend on pork relative to other staples. Second, chicken remains a very competitive option at retail and, in part due to lower feed costs, producers have been pushing more product into the market at lower prices. In Q2, the average price of boneless/skinless chicken breast was 42% lower than a year ago, boneless/skinless thigh meat was 19% lower and whole broilers were 5% lower. Finally, retail merchandisers often take a broader view of their protein case. Pork offers attractive margins while beef drives dollar sales, and retailers seek to balance both rather than simply substitute one for the other.

Last week, the loin primal was down 9% from a year ago, pork butt was down 8% and picnic was down 27%, with a negative trend for all three. A case can be made that current price levels, combined with seasonally higher supplies in late August and September, may encourage retailers to feature more fresh pork after Labor Day and into October (Pork Month). That remains speculative, however, and similar expectations for the summer failed to materialize. The recovery in bellies and hams was long overdue, and clearly positive, but until fresh pork cuts begin to improve it may be difficult for the cutout, and by extension nearby hog futures, to sustain a broader rally

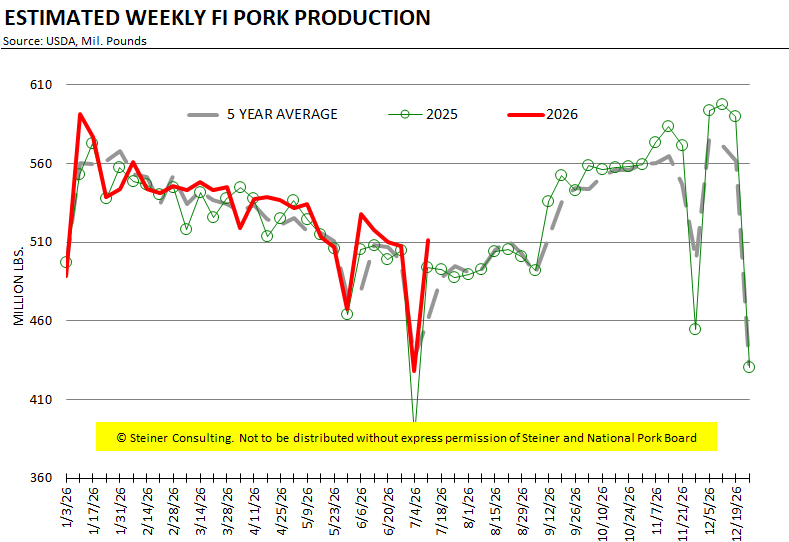

Price Chart

Forecasts

Steiner Consulting Group produces the National Pork Board newsletter based on information we believe is accurate and reliable. However, neither NPB nor Steiner and Company warrants or guarantees the accuracy of or accepts any liability for the data, opinions or recommendations expressed.